One of the biggest misconceptions about long-term care insurance is that it caters exclusively to seniors who may have lost the ability to care for themselves due to age-related impairments. In reality, however, people of all ages can develop conditions or get into accidents that may cause them to need assistance with daily activities. Thus, the need for proper coverage spans across age groups.

This is what long-term care insurance in Canada is designed for. It helps Canadians, regardless of age, cover the huge cost of long-term care if an illness or accident renders them incapable of performing routine tasks.

But how does this type of insurance policy work? What benefits can policyholders get out of it and is it worth taking out? Insurance Business answers these questions and more in this article. For the insurance professionals who frequently visit our site, this would be a good article to pass along to any of your clients, or potential clients who have questions about long-term care insurance in Canada.

In its guidebook, the Canadian Life and Health Insurance Association (CLHIA) defines long-term care insurance as a type of policy designed to provide financial protection if you are unable to care for yourself due to the following:

Depending on the level of coverage, long-term care insurance pays out a portion or all of the expenses incurred in accessing care, which often includes stays in nursing homes and chronic care facilities or the services of a caregiver in your own home.

In general, long-term care insurance in Canada follows either of these two models:

Most long-term care insurance plans also have a waiting period. This is a set time – usually between 30 and 90 days – that must pass before coverage comes into effect. Another important thing to remember is that long-term care insurance benefits are tax-free in Canada.

Long-term care insurance can be complex and involves a lot of buzzwords. If you want to know the meaning behind common industry jargon, you can check out our glossary of insurance terms.

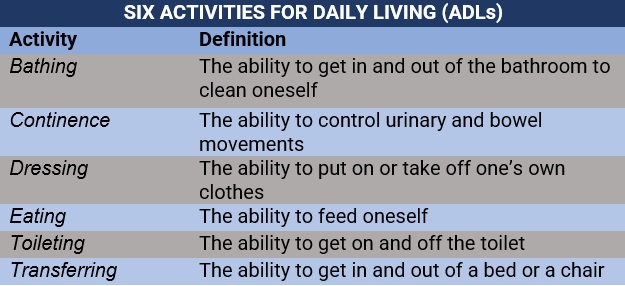

To qualify for long-term care benefits, you will often need to secure certification from a reputable healthcare provider that you can no longer perform at least two of the six “activities for daily living”, or ADLs, in the table below without “substantial assistance.”

You may also be eligible for benefits if you have a debilitating condition, including:

If you file a claim against your policy, your insurer will perform an assessment to confirm your ability to perform these activities. Following confirmation, you can start receiving payments and reimbursements once the waiting period lapses.

Another thing to note is that if you already have a critical illness or disability insurance policy, you may be able to add a long-term care insurance extension without purchasing a separate plan.

Long-term care insurance in Canada covers the cost of care in the following:

Comprehensive long-term insurance policies may also pay out for occupational therapy, rehabilitation expenses, and assistance with personal care tasks, consisting of the six ADLs.

The Financial Consumer Agency of Canada (FCAC) pointed out, however, that long-term care insurance is not only for senior citizens. This type of coverage also protects Canadians, regardless of their age, if an accident or serious condition forces them to require assistance for managing daily activities and prevents them from working for more than 90 days.

This means that instead of supplemental healthcare or therapy draining your savings, long-term care insurance provides you with tax-free benefits to cover the costs.

Canadians who require around-the-clock care have two main options:

Both choices can put a huge dent in your savings. The tables below from CLHIA’s guidebook sum up how much care costs in a long-term care facility and in your own residence in different provinces across Canada.

Depending on the room type and government funding, accommodation in long-term care facilities can start at $900 and exceed $5,000 monthly. The table below shows the monthly average cost for retirement homes without government subsidy.

ACCOMMODATION COSTS, RETIREMENT HOMES/RESIDENCES BY PROVINCE

Jurisdiction

Average cost per month

Private

One-bedroom suite